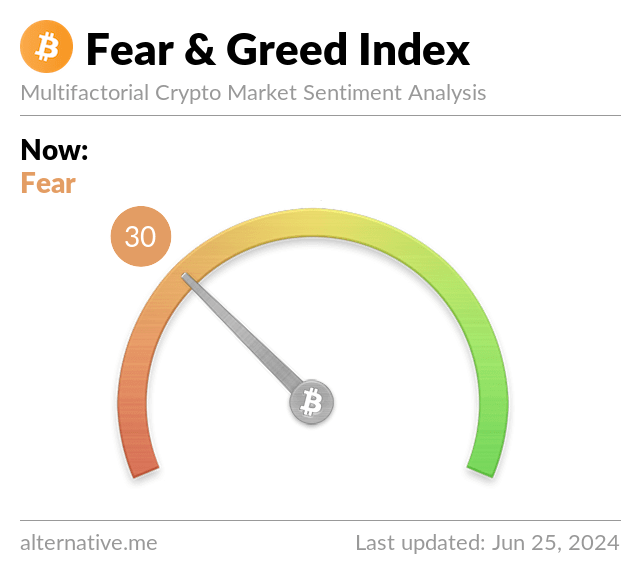

- Crypto Fear and Greed Index is currently in the “fear” zone with a score of 30.

- This is the lowest sentiment measure for Bitcoin (BTC) in nearly 18 months.

The Crypto Fear and Greed Index, a measure of market sentiment for Bitcoin (BTC) and the broader crypto market, has dropped to 30, the lowest score it has reached in over one and half years.

While BTC has traded lower during the current market cycle and the Crypto Fear & Greed Index has fallen into the “fear” zone, this is the first time it has done so since January last year.

Crypto Fear & Greed Index drop to 30

As Bitcoin price slipped below $60,000 on Monday, June 24, the index score nosedived more than 20 points to drop into the “fear” zone.

The decline means the Bitcoin Fear & Greed Index is currently trending at levels last seen in January 2023. At the time, Bitcoin price was trading around $17,000 after the market reaction to the industry’s most shocking collapse so far – the implosion of the FTX crypto exchange.

In May this year, Bitcoin price fell to lows of $56,500 and the index’s score dipped from neutral to fear.

A bounce in price saw sentiment improve significantly to push the Fear & Greed Index to 74. “Greed” dominated then as Bitcoin broke above $71k, but that score flipped neutral and within hours on June 24, reached the 30 mark.

Mt. Gox repayments and German government selling

Catalysts for the latest declines include the Mt.Gox repayments news.

A notice on Monday indicated that the exchange will begin repaying customers who’ve waited since the 2014 hack. Mt.Gox customers will receive Bitcoin and Bitcoin Cash.

Over $8.5 billion worth of BTC is with the exchange’s trustee. In April, analysts at K33 Research warned that Mt.Gox’ Bitcoin repayments could impact prices.

Also attracting negative sentiment is the selling of Bitcoin by the German government. After sending 1,700 BTC to exchanges last week, including Coinbase and Kraken, Germany is at it again.

On Tuesday, Lookonchain shared on-chain data tracking wallets linked to the 50,000 BTC seizure the German government made early this year. The details show another 400 BTC deposited in CEXs.

- Crypto Fear and Greed Index is currently in the “fear” zone with a score of 30.

- This is the lowest sentiment measure for Bitcoin (BTC) in nearly 18 months.

The Crypto Fear and Greed Index, a measure of market sentiment for Bitcoin (BTC) and the broader crypto market, has dropped to 30, the lowest score it has reached in over one and half years.

While BTC has traded lower during the current market cycle and the Crypto Fear & Greed Index has fallen into the “fear” zone, this is the first time it has done so since January last year.

Crypto Fear & Greed Index drop to 30

As Bitcoin price slipped below $60,000 on Monday, June 24, the index score nosedived more than 20 points to drop into the “fear” zone.

The decline means the Bitcoin Fear & Greed Index is currently trending at levels last seen in January 2023. At the time, Bitcoin price was trading around $17,000 after the market reaction to the industry’s most shocking collapse so far – the implosion of the FTX crypto exchange.

In May this year, Bitcoin price fell to lows of $56,500 and the index’s score dipped from neutral to fear.

A bounce in price saw sentiment improve significantly to push the Fear & Greed Index to 74. “Greed” dominated then as Bitcoin broke above $71k, but that score flipped neutral and within hours on June 24, reached the 30 mark.

Mt. Gox repayments and German government selling

Catalysts for the latest declines include the Mt.Gox repayments news.

A notice on Monday indicated that the exchange will begin repaying customers who’ve waited since the 2014 hack. Mt.Gox customers will receive Bitcoin and Bitcoin Cash.

Over $8.5 billion worth of BTC is with the exchange’s trustee. In April, analysts at K33 Research warned that Mt.Gox’ Bitcoin repayments could impact prices.

Also attracting negative sentiment is the selling of Bitcoin by the German government. After sending 1,700 BTC to exchanges last week, including Coinbase and Kraken, Germany is at it again.

On Tuesday, Lookonchain shared on-chain data tracking wallets linked to the 50,000 BTC seizure the German government made early this year. The details show another 400 BTC deposited in CEXs.